Insurance is one of those life expenses that feels unnecessary until it’s needed. At the point that it is needed, however, it’s an expense that can prove its worth and leave people sighing an exhale of relief, for themselves and for their bank account.

Depending on your personal circumstances, some insurance types are more useful than others and it always pays to do your research into individual policies and companies before taking out insurance.

Here are some of the types of insurance that may be worth learning more about.

Health insurance

Private health insurance can help people pay for extra costs that aren’t covered by Medicare if they get sick or injured. It can also offer more choice. With private hospital cover, you can be treated in a private or public hospital, as a private patient. That means you have more options about the doctor that treats you, the hospital you are treated in and a time for treatment that suits you.

People who buy private health insurance can also choose “extras” cover for services generally not included under Medicare like dental, optical, physiotherapy, chiropractic, remedial massage and acupuncture.

And last, but certainly not least, buying private hospital insurance can help people earning over $90,000 a year (or $180,000 for families) avoid an extra tax called the Medicare Levy Surcharge.

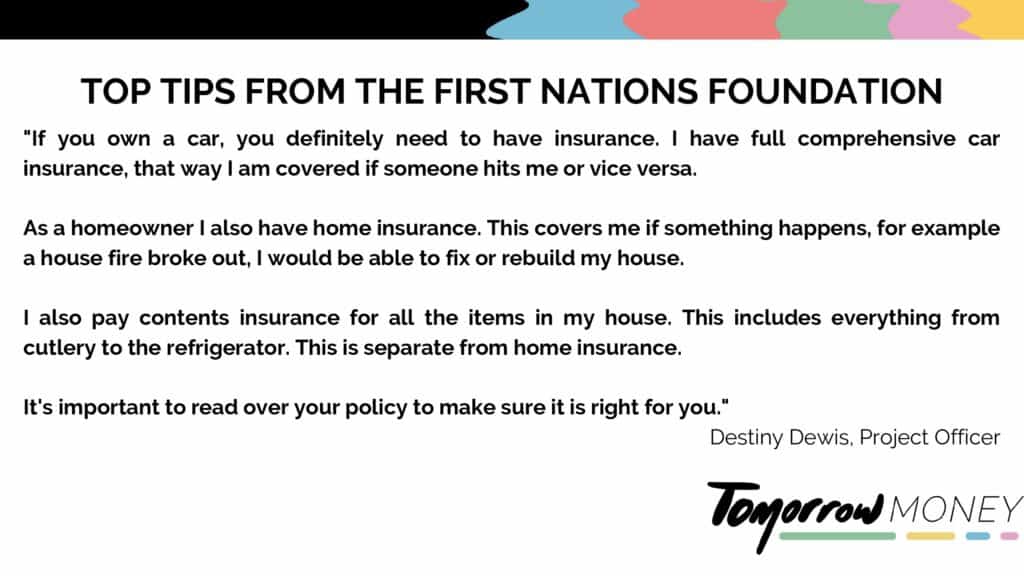

Car insurance

We all know that accidents happen on the road. It is why all car owners should consider whether general motor vehicle insurance is right for them, in addition to Compulsory Third Party Insurance.

Compulsory Third Party Insurance is mandatory in Australia and covers compensation payments for people injured or killed in a motor vehicle accident. But it doesn’t cover the cost of damaged vehicles and property, or damage to – or loss of – your vehicle.

There is also Comprehensive Car Insurance which covers damage to yours and other people’s cars and property, as well as theft. There can be out of pocket expenses payable at the time of a claim, which can vary depending on your age, history and the policy.

Home and contents insurance

With seemingly endless home and contents insurance options, choosing the right policy should come down to a range of factors that make up your personal lifestyle.

For renters, there are specific policies to protect possessions in the event of fire or theft, while landlords may consider taking out landlord’s insurance to cover risks associated with renting out a property.

For homeowners who have a loan, most lenders require some form of home insurance to cover financial loss if there’s damage to the property. Many people group home and contents insurance together to protect both their property and possessions inside.

Some risks may be more relevant to certain people than others, which can be worth thinking about if you buy a home insurance policy. For example, if you live in an area prone to bushfires, you may want to ensure your policy covers you in the case of a fire. If you live where flooding occurs regularly, you may choose a policy that offers flood insurance.

READ MORE: The basics of life insurance

Make it personal

From health to cars to home and contents, choose the policies that best suit your needs.

Putting the time in to find what they are, can reap major benefits in the instance insurance is needed.

Australian Unity is an insurer and a partner of the publisher of this website, the First Nations Foundation.

Editor’s note: Insurance policies are not essential for everyone (except Compulsory Third Party if you drive a car) and it may be worth getting advice before buying a policy you are unsure about. This article is not personal financial advice. To see how much you can afford to spend on insurance, you can use MoneySmart’s budget planner.